Since 1978, real estate properties have increased due to inflation and continued industrial and technological advancements. Land is valuable no matter what occurs, however, the income and financial capacities of clients must be considered during a time like this pandemic.

In this initial Covid-19 stage, investors and analysts have no hard data that reflects current market conditions. All rents and sales that are in contract or have occurred over the past few years reflect market conditions pre-Covid-19.

Very few transactions are being negotiated at this time. It should take three to six months before new leases and sales are closed that reflect our new, albeit maybe temporary, market conditions. Although current market data lack support from closed transactions, values are widely expected to be lower than what is indicated by data from the pre-Covid-19 era.

A flight to quality is now occurring worldwide. U.S. Treasury Bonds and the U.S. Dollar have been beneficiaries during this crisis. In real estate, Net Lease properties appear to be the only property immune to a decline in value. However, the Net Lease market appears to be bifurcated.

Most of the investor interest is directed towards corporate tenants that have top tier credit ratings (Moody’s – A3 and better; S&P – A- and better). These properties are experiencing cap rate compression and thus higher prices.

At the other end of the spectrum are corporate tenants with credit ratings in the B’s or lower. Analysts are forecasting that 40% of corporate bonds rated investment grade will be lowered to junk status. These properties are subject to negative price adjustments as credit ratings are lowered and cap rates rise accordingly.

Yet the two-key question(s) still remain: How far will values erode? How long will the recovery take?

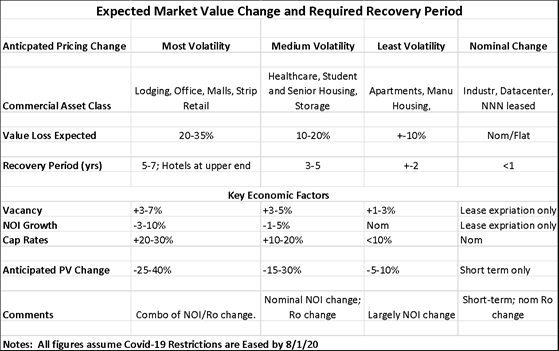

Most analysts have reported the following to date as a general range: 5%-10% for residential; 10% for apartments; 30% for hotels (economy 20%); 5%-10% for industrial; 20%-30% for office; and 25%-35% for retail.The deficiency here is that no recovery timeline is reported.

To these “base” value loss figures, we note that some level of “conversion costs” are likely to be needed post Covid-19 which is not being noted in the marketplace.

Following is an “expectations/value swing” chart along with a corresponding timeline:

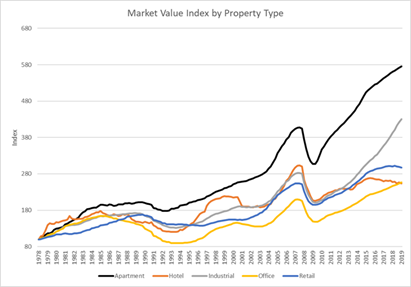

Market Value by Property Type (1978-2019)

Market Value by Property Type (1978-2019)

Exhibit VI, NCREIF

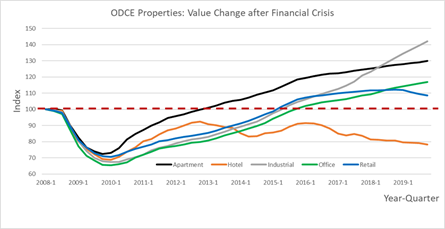

ODCE Market Value by Property Type from Great Recession

Exhibit VII, NCREIF

How Will These Value Expectations Affect Your Real Estate Businesses?

With the expected changes, real estate professionals are encouraged to be vigilant during, before, and after the peak of the Covid-19 pandemic. Expect the changes in real estate values to revert to its previous progression within two years or earlier. Until then, all professionals must continue to study and analyze the data related to values during and after the pandemic. Next, we will look at future variables of real estate values as a result of the Covid-19 pandemic.